Summary of the Production of Clean Hydrogen Credits Under Section 45V of the Internal Revenue Code

The U.S. Department of the Treasury (Treasury Department) and the Internal Revenue Service (IRS) on December 22, 2023, released proposed regulations for the Section 45V Credit for the Production of Clean Hydrogen. The proposal contains rules for lifecycle greenhouse gas (GHG) emissions, verification of projects, and modification/retrofitting of clean hydrogen facilities in relation to the tax credit.

Highlights

- Lifecycle GHG emissions will be calculated through the point of production (well-to-gate) using the most recent version of the 45VH2—GREET (Greenhouse gases, Regulated Emissions, and Energy use in Technologies) model, considering hydrogen production pathways and feedstocks included in the new 45VH2-GREET model.

- Taxpayers can show that electricity used in the hydrogen production process is from a specific source, rather than the grid, by acquiring and retiring Energy Attribute Certificates (EACs) for each unit of energy produced and used. Eligible EACs are to be recorded through a registry/accounting system and meet requirements on incrementality, temporal matching, and delivery.

- Third-party verification of the production and sale of the hydrogen is required for each tax year. Verification is also needed for EACs purchased and retired.

- Credit for facility modification applies to facilities that did not produce clean hydrogen before January 1, 2023, or were modified to be able to produce under 4 kilograms CO2e per kilogram of hydrogen.

- There are no proposed rules relating to renewable natural gas (RNG) used to produce hydrogen, although the final rules may require that for an emissions value to be consistent with the RNG/fugitive methane used, the gas must originate from the first productive use.

- A Qualified Clean Hydrogen facility is defined as a single production line used to produce hydrogen to the point of production.

- Section 45V credits are available for hydrogen produced in the U.S. or a U.S. territory and sold or used within or outside the U.S.

Comment Period

Comments on the NPRM are due by February 26, 2024. Given the need for additional clarity and guidance from Treasury/IRS on key issues, EcoEngineers is available to assist you with the analysis of the proposed regulations and the preparation of comments. Areas to focus on in written comments include the impact of the proposed regulations on project development plans, including how the proposed regulations may result in revised investment decisions, with associated impacts on domestic manufacturing, jobs, and participation in Regional Clean Hydrogen Hubs.

For more information, please contact Tanya Peacock, Managing Director, Hydrogen, at tpeacock@ecoengineers.us.

Full Summary

Proposed regulations for the Section 45V Credit for Production of Clean Hydrogen were released on December 22, 2023, containing rules for lifecycle GHG emissions, verification of projects, and modification/retrofitting of clean hydrogen facilities in relation to the tax credit. Comments on the proposed rule must be received by February 26, 2024. A proposed hearing is scheduled for March 25, 2024, at 10 a.m. ET. Requests to testify must be received by March 4, 2024.

READ MORE: The U.S. Department of Energy’s H2Hubs Program: Accelerating the Clean Hydrogen Economy

In addition to the Notice of Proposed Rulemaking (NPRM), the Administration released the new 45VH2-GREET 2023 model and accompanying manual, a letter from the U.S. Environmental Protection Agency (USEPA) that outlines guidance to the Treasury Department regarding reference to the Clean Air Act in 45V, and a U.S. Department of Energy (DOE) whitepaper that supports the approach taken in the proposed regulations to assessing the lifecycle GHG emissions of electricity used to produce hydrogen.

Taxpayers may rely on these proposed regulations for taxable years beginning after December 31, 2022, and before the date the final regulations are published in the Federal Register, provided taxpayers follow the proposed regulations in their entirety and in a consistent manner.

Determination of Lifecycle GHG Emissions

Lifecycle GHG emissions will be calculated through the point of production (well-to-gate) using the most recent version of the 45VH2—GREET model. Factors considered in lifecycle emissions include feedstock growth, gathering, extracting, processing, and delivery to the facility, and emissions in the production process, including electricity used and carbon capture and sequestration (CCS) done by the facility.

The “most recent version” of the 45VH2-GREET model is considered the model that is publicly available on the first day of each taxable year of which the hydrogen claimed under 45Q was produced. If a newer version is available after the first day of the taxable year, it can be used at the taxpayers’ discretion.

Hydrogen Pathways and Feedstocks

Hydrogen production pathways and feedstocks included in the new 45VH2-GREET model include:

- Steam methane reforming (SMR) of natural gas, with potential carbon capture and sequestration (CCS)

- Autothermal reforming (ATR) of natural gas, with potential CCS

- Steam methane reforming (SMR) of landfill gas with potential CCS

- ATR of landfill gas with potential CCS

- Coal gasification with potential CCS

- Biomass gasification with corn stover and logging residue with no significant market value with potential CCS

- Low-temperature water electrolysis using electricity

- High-temperature water electrolysis using electricity and potential heat from nuclear power plants

Petitions can be filed for a Provisional Emissions Rate (PER) if the GHG emissions rate for feedstock or production technology is not included in the most recent GREET model. An emissions value will have to be requested from the DOE and then included with a PER petition. Following acceptance of the emissions value and PER, the emissions value may be used to calculate credit under 45V. The PER process will only address hydrogen production pathways using biogas and RNG not included in the 45VH2-GREET 2023 model after the final regulations are issued.

Electricity and Energy Attribute Credits (EACs)

Taxpayers may show electricity used in the hydrogen production process as being from a specific source, rather than the grid, by acquiring and retiring EACs for each unit of energy produced and used. Renewable Energy Certificates (RECs) are included as a form of EACs. Eligible EACs are to be recorded through a registry/accounting system and meet requirements on incrementality, temporal matching, and delivery.

To meet the incrementality requirement, the electric generating facility that supplies the electricity that the EAC is based upon must have a commercial operations date (COD) that is no more than 36 months before the hydrogen production facility is placed in service. An alternative test is the requirements may be met if the electricity generating facility has not had an uprate (increase in nameplate capacity) more than 36 months before the hydrogen facility was placed in service and that electricity is part of the uprated production. Other approaches are also being considered such as an avoided retirement approach, a zero or minimal induced grid emissions approach, and a formulaic approach that would allow a fixed percentage of electricity from all existing clean power generators to qualify based on expected curtailment rates. The Treasury Department is seeking comments on these approaches.

The temporal matching requirement may be met by demonstrating that the EAC is generated within the same hour that it is consumed by the hydrogen facility. However, there is to be a transition rule in place, as the ability to track by the hour is currently limited. Until 2028, the transition rule will allow annual matching.

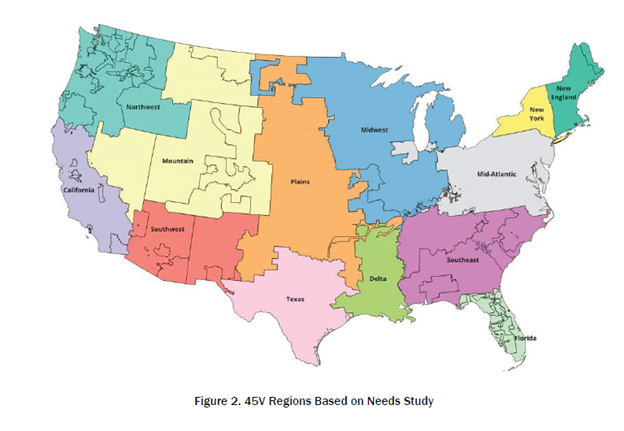

The deliverability requirement is met if the EAC electricity is generated by a source in the same region as the hydrogen facility. “Region” is defined as the U.S. regions defined in the DOE Needs Study. The region hydrogen facilities and generating sources are located is based on the location of the balancing authority to which it is electrically interconnected. The Treasury Department is seeking comments on whether the regions are appropriate as designed, per the table shown below.

Verification of Production and Sale

Third-party verification of the production and sale of the hydrogen is required for each tax year. Verification is also needed for EACs purchased and retired.

A verification report is to include product attestation, sale or use attestation, conflict attestation, a qualifier verifier statement, general information about the facility (location, production description/method, feedstock, amount of feedstock used, list of metering devices and statement on quality control/calibration/activation), and documentation to substantiate the verification process.

A ”qualified verifier” is an individual or organization with active accreditation as a validation and verification body from the American National Standards Institute (ANSI) National Accreditation Board (ANAB), or a verifier, lead verifier, or verification body under California’s Low-Carbon Fuel Standard (LCFS) program. EcoEngineers has been granted accreditation from ANAB, in accordance with the International Organization for Standardization (ISO) standards ISO/IEC 17029:2019 Conformity assessment — General principles and requirements for validation and verification bodies.

Modification of an Existing Facility

Credit for facility modification applies to facilities that did not produce clean hydrogen before January 1, 2023, or were modified to be able to produce under 4 kilograms CO2e per kilogram of hydrogen. The date placed into service for modified facilities will be changed to the date the property required to complete the modification is placed in service. Existing facilities may have the date placed into service updated to the date that new property is added, so long as the used property is not more than 20% of the facility’s total value (80/20 rule). Replacing natural gas with biogas or renewable natural gas in the hydrogen production process does not qualify as a facility modification under the proposed rules.

RNG and Fugitive Sources of Methane

There are no proposed rules relating to RNG used to produce hydrogen, though it is suggested that the final rules may require that for an emissions value to be consistent with the RNG/fugitive methane used, the gas must originate from the first productive use. Otherwise, the gas would be given an emissions value consistent with natural gas. Attribute certificates would need to be acquired and retired to demonstrate procurement of the gas and that environmental attributes are not being sold to other parties or used for compliance with other policies and programs. Additionally, hydrogen producers would be required to have a pipeline interconnection and measurement using a revenue grade meter. There are 12 questions listed in the proposed rules asking for comments relating to RNG/fugitive methane used in hydrogen production.

Additional Rules

A Qualified Clean Hydrogen facility is defined as a single production line used to produce hydrogen to the point of production. A single production line is defined as all components of property that function interdependently to produce hydrogen. Electricity production equipment is not included in the definition of a facility. Components with purpose in addition to the production of hydrogen may be part of the facility if they function interdependently with other components to produce the hydrogen.

READ MORE: Life-Cycle Analysis and Clean Hydrogen Consulting

The “taxpayer” is who owns the hydrogen facility at the time of production to which the credit is claimed, regardless of if they are the “producer.” Credit is determined for all produced in a hydrogen taxable year, regardless of whether verification or sale of produced hydrogen occurred in that year. Still, the credit cannot be claimed until verification occurs. Thus, the taxpayer would have to file an amended return or administrative adjustment if verification occurs after the return filing deadline.

An anti-abuse rule is to be implemented to make credit unavailable if the purpose is to produce in a wasteful way. This includes if the taxpayer knows, or has reason to know, that the hydrogen produced is to be vented, flared, or used to create additional hydrogen.

Section 45V credits are available for hydrogen produced in the U.S. or a U.S. territory and sold or used within or outside the U.S.

For more information, please contact Tanya Peacock, Managing Director, Hydrogen, at tpeacock@ecoengineers.us.